If you are just starting your career or if your credit scores have fallen below an acceptable point, getting loans for large items like a car or a house can seem nearly impossible.

Companies do not want to sell their products to people who may not be able to pay for them. Since your credit score is a rating of how reliable you are with making payments, you may find yourself in a tight spot while asking for a loan with poor credit.

One way around bad credit scores is to have someone cosign a loan with you.

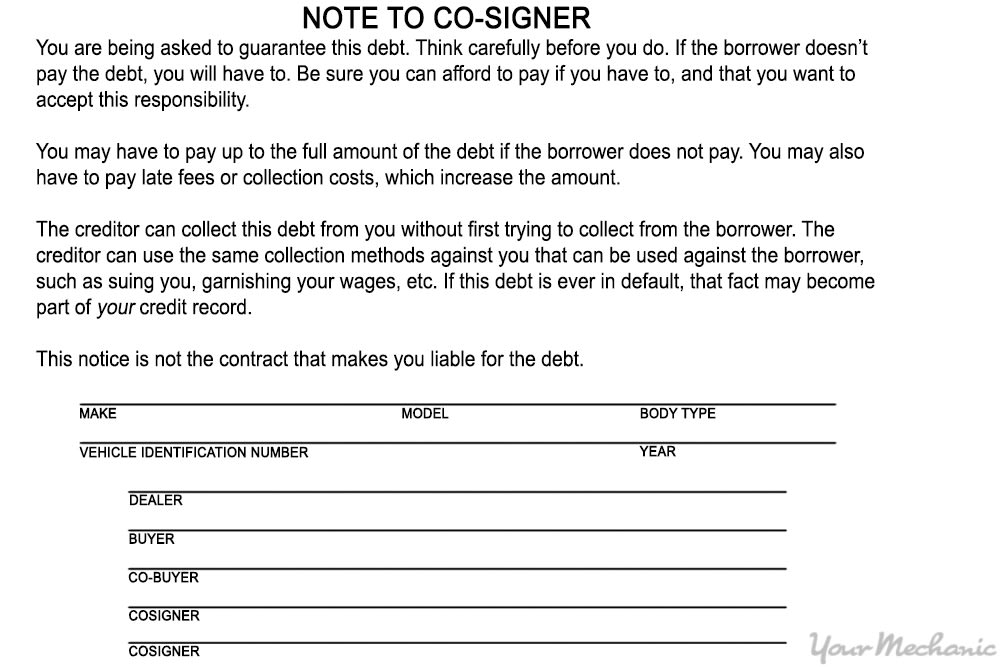

A cosigner takes on a lot of responsibility, but in many cases this is necessary for the lender to make a deal with you. If you cannot make a loan repayment, the cosigner will be billed the full amount and they will be expected to make the payments instead of you.

Part 1 of 1: Find a cosigner for your car loan

Step 1: Decide if getting a loan with a cosigner is right for you. Generally, you should only be buying and/or financing items that you can afford. If you can afford a certain car, then you should be able to finance it without a cosigner.

Here are some points to keep in mind before pursuing a loan with a cosigner:

Buy a used car: You can probably afford a cheap used car if you can afford to finance a new car. With a used car, then value does not drop as much from use so it is less likely that you’ll owe more than the car is worth on the loan.

Take time to build good credit: Hold off on buying a car, if possible, and take some time to build a good credit score. If your score is already low, speak with a financial advisor about ways in which you can rebuild your score.

A bad credit score, while not always completely the fault of the individual, is indicative of irresponsible financial behavior. Consider whether or not buying a car is a good idea given your current finances.

Make regular payments to build credit: If you have not built up much credit but still really need a reliable car, then buy an inexpensive, lightly-used car. A cosigner would be necessary, but as long as regular payments are made then this is a good opportunity to build some good credit.

Get a loan with unfavorable terms: In some cases, people with mediocre credit scores will get approved for a loan with bad terms or a high interest rate. In cases like these, a cosigner could reasonably assume that payments would be made, seeing as the person was already budgeting for a monthly loan payment.

Step 2: Prepare to apply for a loan. Gather the information necessary for applying for a loan in the first place.

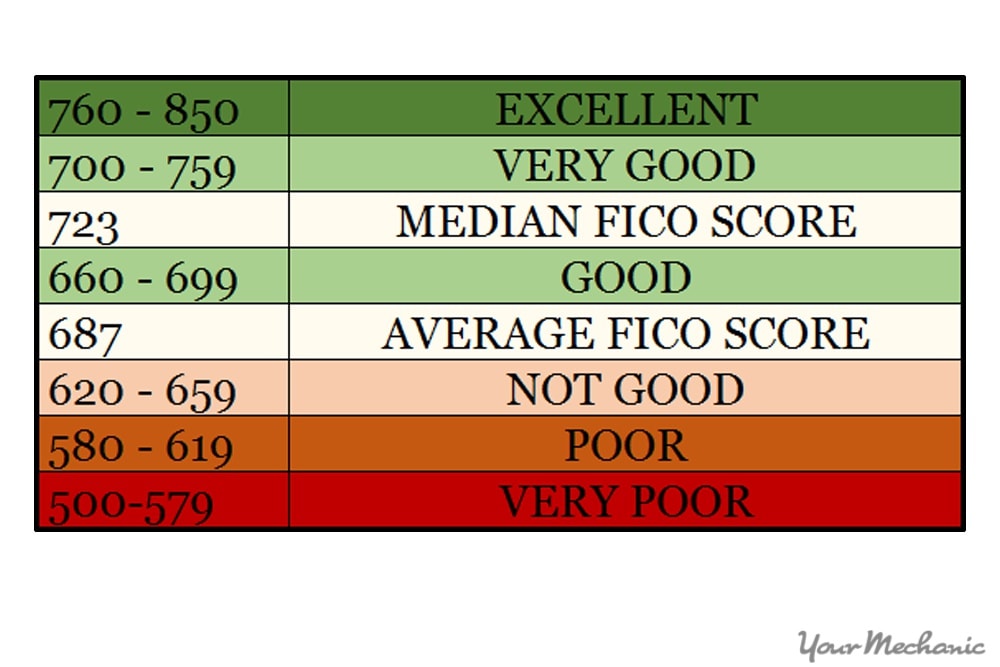

Use an online service of your choice to find out your credit score and see where you stand using that metric.

A score below 700 will make negotiating good terms difficult, and a score below 350 will make getting a loan nearly impossible.

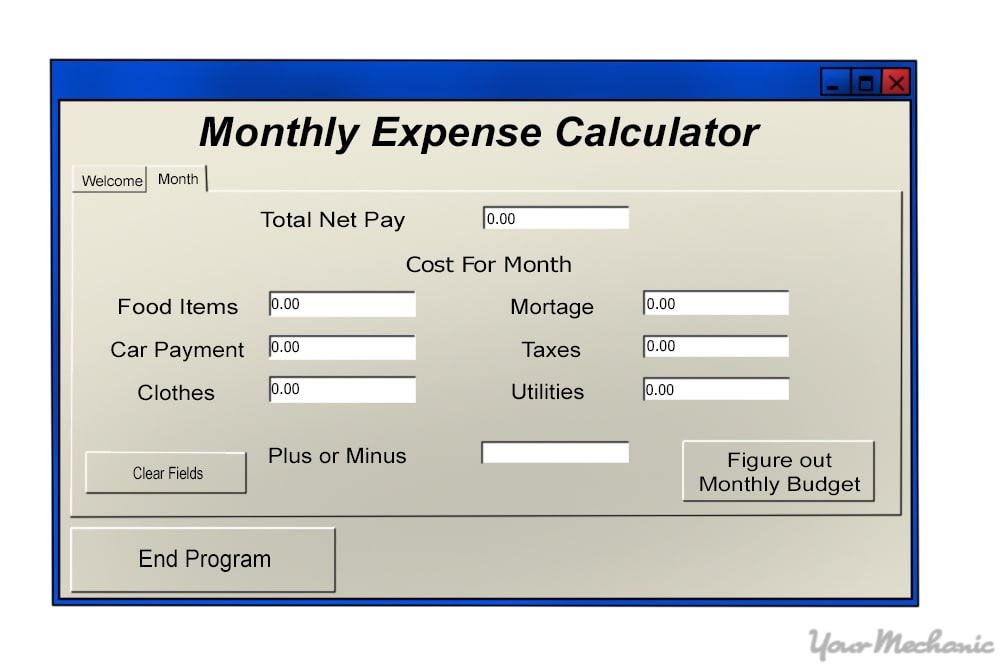

Calculate your monthly income and what your expenses are. Using this, you should be able to calculate what amount of money you can spare each month for loan payments.

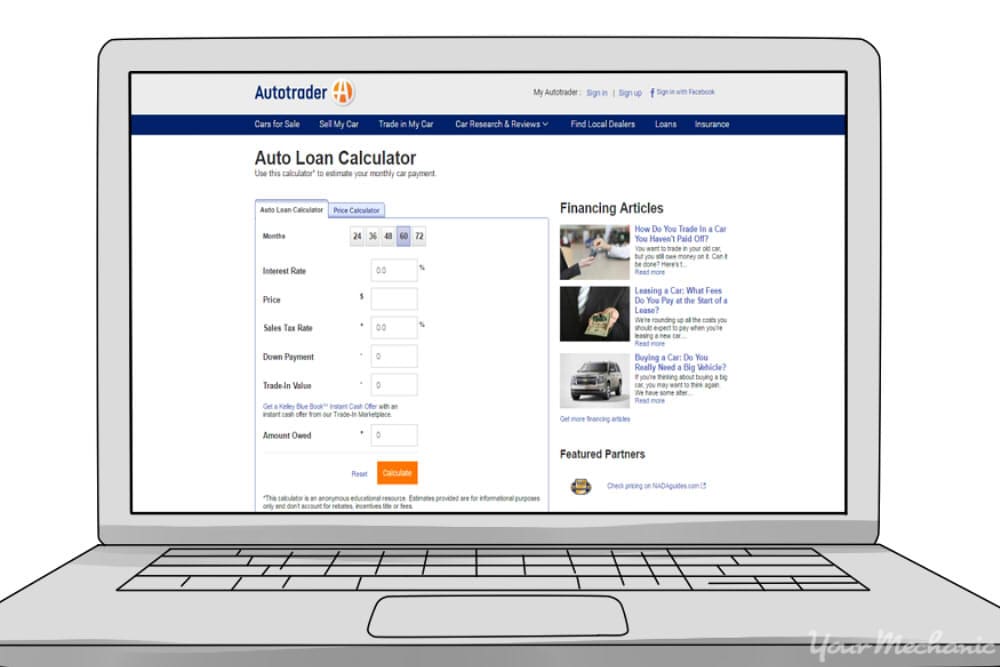

Find a few different models of car that would result in payments that are within the range you can afford. This will save time and energy when you are at the dealership searching for a car.

Step 3: Find a cosigner. While this may sound like one of the simpler steps in the process, it is very important to slow down and really read through all of the numbers involved before finalizing the decision with your cosigner.

Will you be able to afford these payments in the long term? If you are young, you may miss opportunities in the future because you could not take a pay cut or stop working to attend school without defaulting on the loan.

Think of the amount of money being spent as one big sum. Say it’s $15,000. How long would it take you, starting right now, to earn that much? Now add to that the fact that interest will increase the original figure over time.

Consider what would happen if you could no longer pay the loan and the cosigner had to take over payments. How would that affect them? Would they even be able to afford the whole payment themselves?

Loved ones usually end up being the ones to cosign on a loan with you, so there may be more at risk than a bad credit score if the loan goes unpaid. Serious tension and family drama has stemmed from loans being cosigned.

Sit and talk with the cosigner and set a budget that not only works for you, but works for their budget in case they end up taking over payments. This may reduce the amount you have to spend on a car, but it is better than signing a predatory loan agreement.

Step 4: Determine your price range. Pick out a car that is in your price range when tax is included in the price. Look at the total sum of money that is being loaned and imagine what it will be like making that extra expense every month.

If your expenses are $900 a month and you make $1,600 a month, then a $300 car payment may make you have to choose between having an active social life and having a savings account.

Your employment has to be stable enough to pay this amount until the car is totally paid off. It is easy to change jobs or even fields in four or five years, so keep that in mind when considering a loan.

Once you and your cosigner come to an agreement on the sum of money being paid and the terms of the loan, sign the paperwork and get on the road!

You may need the assistance of a cosigner in order to qualify for the credit you require. It’s very important to manage a cosigned account wisely. Ensure that you make your payments as agreed each and every month.

Remember, your cosigner is doing you a big favor and if you fall behind on payments, the delinquency will show up on your cosigner’s credit report as well as your own.