Very few people have the money on hand to purchase their vehicle outright. Vehicle financing is in place to give purchasers the option of borrowing money from a lending institution. Whether you have good credit, bad credit, or no credit, there is almost always a lender willing to provide you with a car loan.

Sometimes you have to accept finance terms that aren’t the best. That might be because you have a poor credit rating or no credit rating, your vehicle purchase exceeds your affordability on paper, or you don’t have time to shop around for a better interest rate or term length.

You may find you can save money or lower your payments if you refinance your vehicle. Learn the steps you should take to find the best deal on your refinance.

Part 1 of 2: Determine if refinancing is the right move for you

Step 1: Decide why you want to finance. If you’re looking for lower interest rates or lower payments, you will want to find a lender who will offer that for you.

Step 2: Check your credit score. Figure out your credit score from a reputable source.

If it has improved from when you first financed, you may qualify for a better interest rate. If the score has stayed the same or even dropped, you may qualify for lower payments, but the interest rate may be higher.

- Tip: You may want to work on your score before applying.

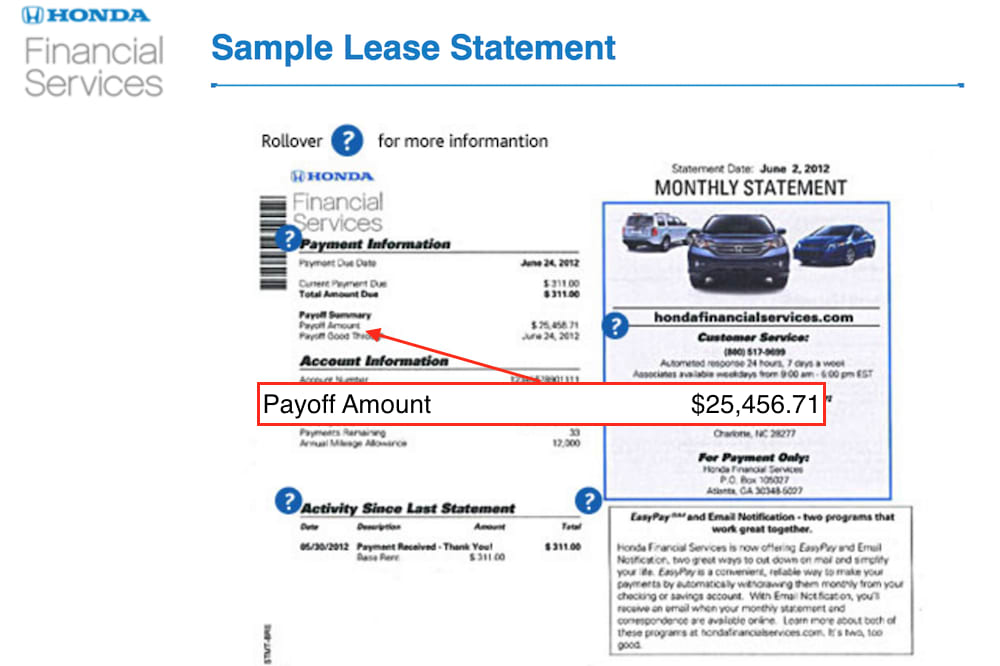

Step 3: Find out the balance on your current car loan. You’ll need to provide this amount to other lenders when you’re looking to refinance.

Contact your lender to verify the current payoff amount, and ask if there are any fees for early loan disbursements.

Step 4: Compare interest rates. Find out current interest rates on a refinance loan and compare them to what you’re currently paying.

If the rate is within only a few points of your current rate, you may not benefit by refinancing after paying any loan disbursement fees.

Step 5: Calculate your budget. This will help you to determine how much you can afford to pay.

This is an important step whether you’re looking to refinance to lower payments or to reduce the amount you have to pay by increasing your monthly payments. Calculate the monthly or bi-weekly amount you can afford, not the overall loan amount.

Step 6: Make a decision on the refinance. Decide if refinancing will help you meet your goals or if you should wait.

You may need to get caught up on your car loan payments or improve your credit score.

Part 2 of 2: Find a new loan

Step 1: Check with your lender. Reach out to your lender if your circumstances have changed.

They may be able to offer you a new loan at a better rate of lower monthly payment.

Step 2: Compare other lenders and loan products. Don’t settle for the first lender who approves you for a loan.

Avoid filling out an application and having your credit score pulled until you decide if the loan terms are agreeable.

Step 3: Check with local banks and credit unions. Local lenders often offer lower interest rates, especially if you originally financed through the dealership.

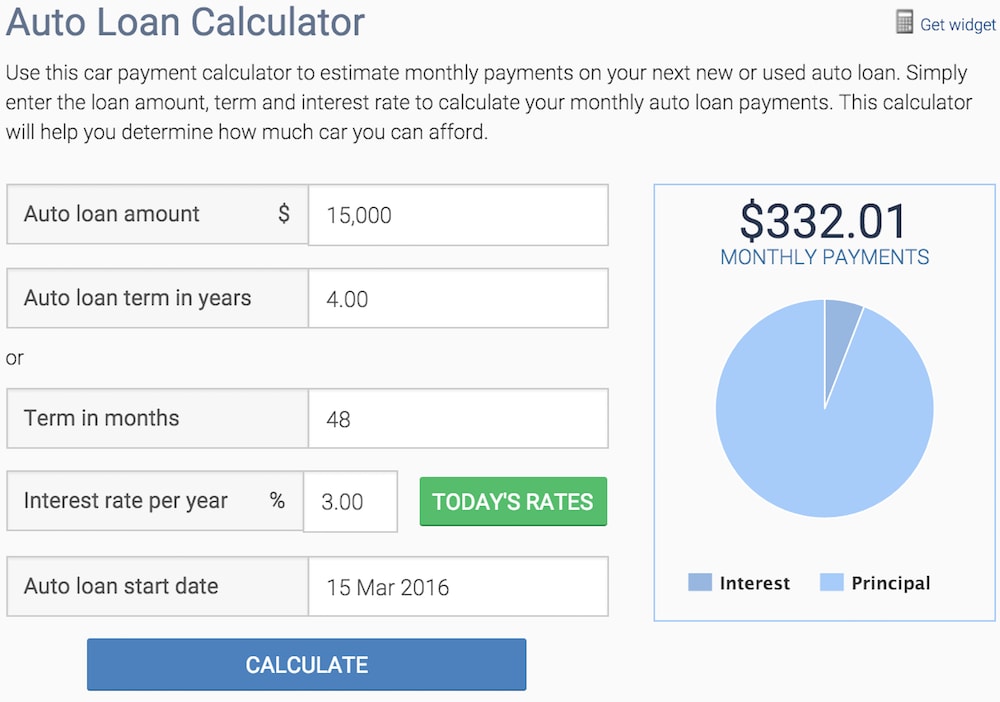

Step 4: Check online for auto refinance loans. Look online to compare interest rates and length of the loans to determine if they benefit you and which one is best.

You can use an online tool to help you make an informed decision.

Step 5: Fill out the application. Once you have selected the loan you want, fill out the application.

Step 6: Contact your old lender. Once you have been approved, contact your old lender to get the details and pay off your first loan.

Some lenders will issue you a check while others will pay the lender directly.

- Tip: Check the Better Business Bureau to see if any complaints exist for the lender you’re considering.

Whatever the reason, refinancing may be a feasible option to put you in a better financial situation. While there may be a lot of concern about the process, there is no reason to think that it cannot be a straightforward and rewarding one. Be sure to keep your car on a regular maintenance schedule so your investment pays off.