If you have sold a car but the buyer has breached the terms of the contract, then you are allowed to repossess the vehicle. Repossessing your car means that you reclaim it as your own due to the failed contract or lack of payment from the new owner.

If the person you sold your car to is not complying with their contractual obligations, then you are eligible to repossess the vehicle immediately.

In theory, repossessing a car is simple; you just take the car back, and then do with it what you please. However, the process of a repossessing a car successfully and legally can sometimes be tricky, so it’s imperative that you go about it correctly.

Method 1 of 2: Repossess the car on your own

Step 1: Locate the car that you want to repossess. If you know the buyer of your car, it may be easy to locate the vehicle.

However, if the buyer is aware that you are going to attempt to repossess the vehicle, then they may be evasive, or have the car hidden from you.

One of the best places to look for the vehicle is at the buyer’s place of employment, as that is usually a public area, and easy to find. If you cannot locate their place of employment, the best approach is to visit the buyer’s home address (which you should have from the selling process).

Step 2: Approach the vehicle when it is in a public place. The right to repossess your car does not come with the right to breach the peace.

In other words, you cannot disturb or damage the buyer or the buyer’s property when repossessing your car.

Note: If you locate the car in the buyer’s closed garage or gated driveway, for instance, you are not allowed to break and enter to get the vehicle. Instead, wait until it leaves the private property, and is in a public area. This may mean you have to wait outside the buyer’s home until they leave with the car, and then follow them to wherever they park.

Warning: If you breach the peace while repossessing the vehicle, then the buyer is eligible to sue you.

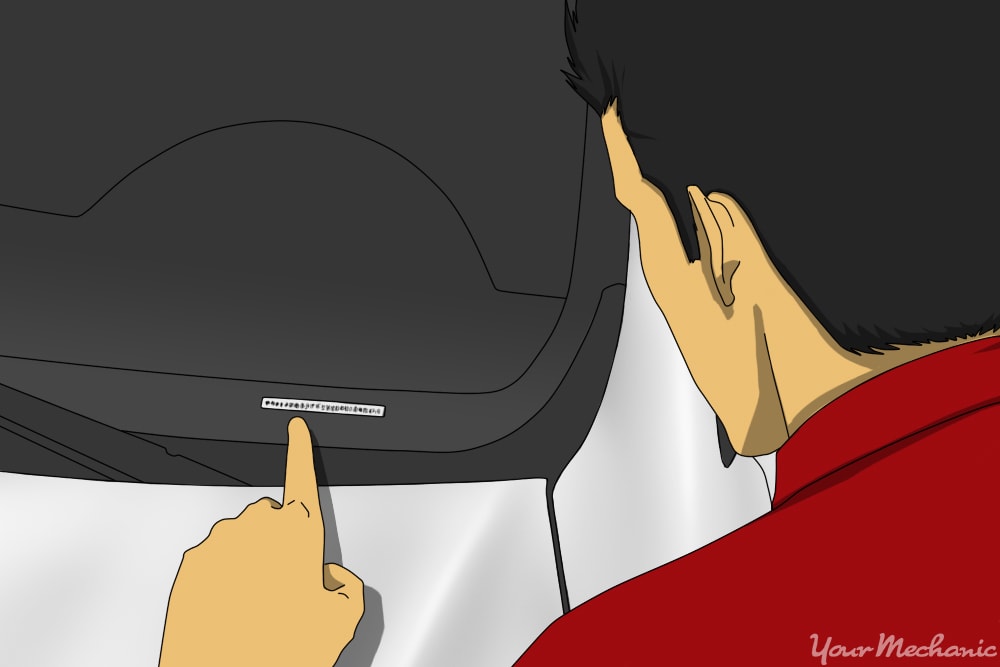

Step 3: Verify the VIN. Once you have found the car, check the vehicle identification number (VIN), to make sure that it is actually the one you are trying to repossess.

The VIN is located at the front driver’s side corner of the dashboard, and is visible through the windshield.

Warning: If the VIN is not that of the car that you sold, then it is not the correct vehicle, and attempt to repossess it would be theft.

Tip: Before searching for your vehicle, make sure that you have the correct VIN information on hand.

Step 4: Repossess the car. There are countless ways to take the vehicle back into your possession. You can tow the car yourself, or hire a towing service to tow it for you.

You can use the key code that came with the vehicle to have a spare key made, and use that to enter the vehicle. You can also pick the lock, or call a car service to help you enter the vehicle in the same way that you do when you lock your keys in the car.

Step 5: Check the condition of your vehicle. Make sure that the vehicle is in the same condition as when you sold it.

After repossessing your car, hire a certified mechanic, such as the ones at YourMechanic, to perform an inspection. If your car has been damaged since you sold it, you will be eligible to receive payment from the buyer.

Method 2 of 2: Use a repossession specialist

Step 1: Hire a repossession specialist. If you are not comfortable repossessing your vehicle on your own, or if you do not have the time to do it, then you can hire a repossession specialist.

After giving the specialist the VIN and the buyer’s information, the specialist will then repossess the vehicle for you.

- Tip: Make sure to do your research and only hire a repossession specialist that is reputable and has positive reviews.

Step 2: Check the condition of the repossessed vehicle. Just like when you repossess the vehicle yourself, you’ll want to check the condition of the vehicle after a repossession specialist has returned the car to you.

If the car is in noticeably worse shape than when you bought it, you will be eligible to receive compensation.

After repossessing your vehicle, you can keep it as your own, or you can sell it to a new buyer. If you opt to sell the vehicle once again, then you can receive a deficiency balance, depending on what you sell the car for.

A deficiency balance is the difference in the original selling price, and the price you got paid. For example, if you agreed to sell the car to the first buyer for $20,000, but only received $2,000 before you repossessed the vehicle, and then re-sold it for $15,000, then you are still $3,000 short of the initial agreed upon price. You are therefore entitled to a $3,000 deficiency balance from the original buyer.

Furthermore, you can also re-sell the vehicle to the original buyer, as long as they work with a loan service to pay you in full, so that the issue does not arise again.