Sometimes businesses need access to a vehicle on a regular basis, or even occasionally, to serve its customers. Purchasing a car under your business name that employees can drive often saves companies time and money versus reimbursing employees for driving their own personal vehicles. Buying a vehicle under a business name can take some time, but by following some simple instructions, you can make your next car purchase for your business stress-free.

Part 1 of 5: Build your business’ credit rating

The first step to ensuring that you can qualify for a business loan to buy a vehicle is to ensure that your business’ credit rating is the best it can be. Like an individual, businesses can build credit by paying bills on time, whether through small loans or obtaining a business credit card and paying it off regularly.

Step 1: Apply for a small loan. Start out small and get a small business loan, making sure to always pay the monthly payments on time. The loan does not have to be large, and your company might be best served if the loan is small enough that you can pay it off within a few months.

Step 2: Get a line of credit. You should also consider applying for a business line of credit. Credit cards are the easiest way to build your business' credit rating. Just make sure to make your payments on time.

Step 3: Get an EIN. Provide your business' employer identification number (EIN) to all vendors and other companies you conduct business with and ask them to report your credit accounts to Dun & Bradstreet or Experian. This helps your company establish credit under the EIN instead of using your personal Social Security Number.

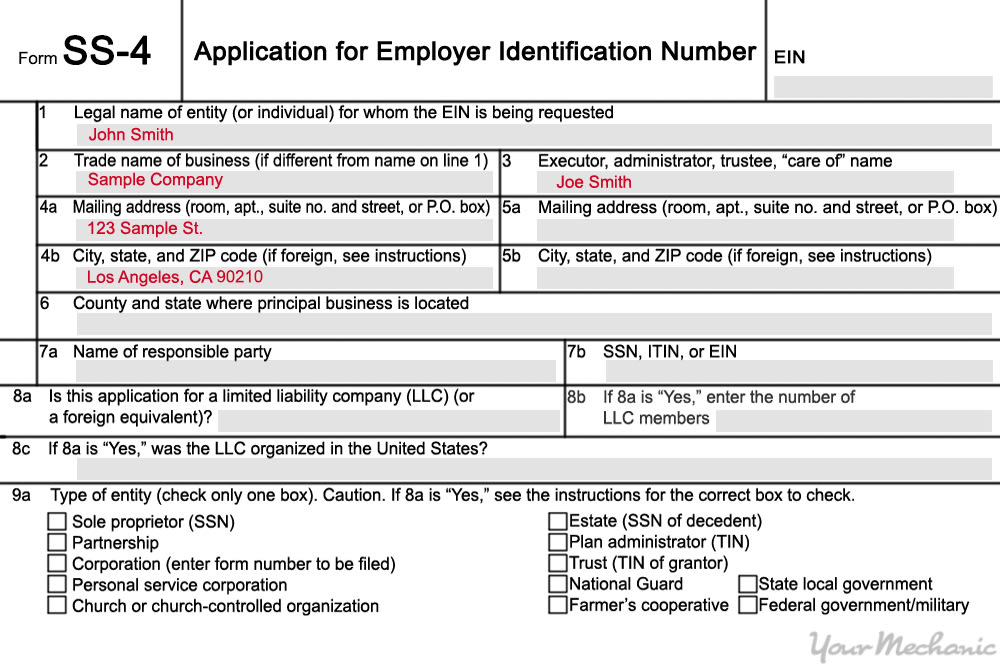

An EIN is provided by the government. It acts the same for a business as a Social Security Number does for an individual. Lenders, vendors, and government agencies will use your EIN to identify company transactions at tax time, including to verify that your company purchased a vehicle. If you are still in the stages of setting up your business and do not have an EIN number yet, follow these steps to do so:

Fill out the IRS form SS-4, which establishes an EIN for a company. You can find it on the IRS website. If needed, you can find resources to help you properly fill out the EIN paperwork online.

After you get your EIN number in the mail from the IRS, list your business with your state, including the new EIN.

Part 2 of 5: Prepare a loan proposal

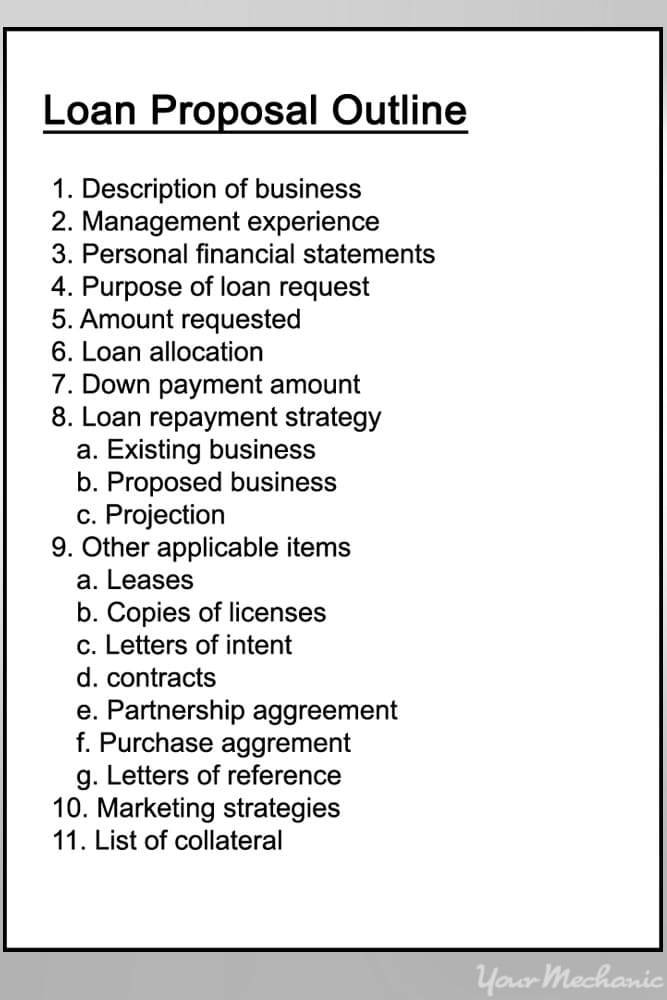

After you have obtained an EIN for your business and established a good credit rating, it is time to make the loan proposal for the vehicle you want to acquire through your business. The loan proposal contains such information as why your company needs the vehicle, who will use it and for what purpose, and the information about the loan amount you need. This loan proposal helps show lenders, either at a bank, via online lenders, or through dealership financing partnerships, that you have a solid understanding of the marketplace, as well as possess strong management skills.

Step 1: Draft a proposal. Start writing out the loan proposal. Any lender you approach needs to know why your business needs to purchase a vehicle. Any time a lender loans a business money, they have to look at the risks involved and whether a vehicle purchase makes sense for your business.

Step 2: Document all drivers. In addition, make sure to document who will use the vehicle. Whereas the use of a vehicle by the business owner's wife might not be a good enough reason, it is if she is a salesperson for the business and needs it to visit clients in person. Be specific in who plans on using it and for what purposes.

Step 3: Calculate how much money you'll need. When seeking a loan for a vehicle for a business, lenders also need to know how much money you need. You should also state how much you have as a down payment for the loan and if you have any collateral.

- Tip: As a part of your loan proposal, make sure to mention what your company's marketing strategies are, as well as the past and current performance of your business. This can help build a case with the lender about how good an investment your company is overall.

Part 3 of 5: Find a car dealership with a commercial division

Look for a dealership with a dedicated commercial sales division. They will be more knowledgeable about selling cars to businesses, which helps ensure transactions run smoothly and that you get the best deals.

Step 1: Research dealerships. Investigate the various dealerships in your area to find one that finances and sells cars to businesses. Many of these will offer special programs and even fleet discounts if you purchase multiple vehicles.

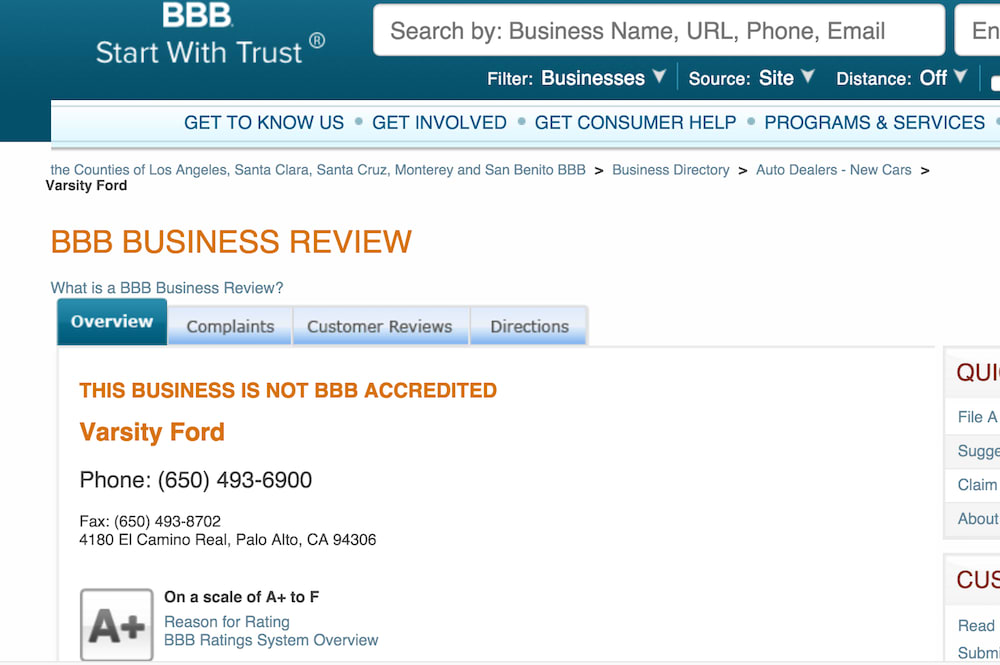

Step 2: Compare dealerships. Check out their ratings using the Better Business Bureau. This can help weed out dealerships with bad customer ratings.

Step 3: Ask for recommendations. Ask other businesses with company vehicles where they made their purchase. You can also look for online testimonials from other businesses for a particular dealership.

Step 4: Browse the inventory. Visit the websites of the dealers to see what inventory is available and if they list a commercial division with details for businesses purchasing vehicles. You should also compare the prices of the various dealers you have an interest in using, and while it should not be the deciding factor, price should play an important part.

Part 4 of 5: Narrow down the list of lenders

You also need to gather a list of lenders that you are interested in using to provide the money to purchase the vehicle. You should base your list of lenders on what interest rates they offer and the terms of any loan. Finding a viable lender is an important part of the process, as a lender has to approve you for the loan. That is why it is important to make sure your credit rating is in good order before approaching any lenders.

Step 1: Find a lender. Research which companies offer loans for businesses. Some of the most popular lenders include:

Banks where you have your business accounts. See if they offer special rates for businesses that have an account with them.

Online lenders that specialize in business car loans.

A larger dealership that has a loan department.

Step 2: Pick your best options. Narrow the list down to the three who offer the best rates and terms. Do not get rid of your larger list as you might not qualify with your first choices of lenders.

Step 3: Find out lenders' requirements. Call the lenders on your short list and ask them what they require when it comes to a business' credit rating and history. Be prepared if you do not qualify for a loan with the lender due to your credit rating and business history.

Step 4: Be persistent. If your first choices do not work with your current credit and business history, you need to go back to your list and choose at least three more to call. Continue going down the list until you find a lender who offers terms and interest rates you can live with.

- Tip: If your business has been established for some time, you’ll probably have no problem getting a car loan. If your company is new with no credit history, you may have to do more searching to find a willing lender.

Part 5 of 5: Finalize the loan

The final step in the loan process after finding the vehicle or vehicles you want includes providing all of the necessary paperwork. Once the lender has taken a look at your paperwork, including the loan proposal, they can either approve or deny your loan. If they accept your loan, all you need to do is fill out and sign the lender's paperwork.

Step 1: Negotiate the price. After you have found a lender you are satisfied with, negotiate the purchase price of the vehicle you have chosen. Be willing to increase the amount of down payment to offset any lack of credit history.

Step 2: Organize your documentation. In addition to your loan proposal, provide documentation for your business, including a balance statement, profit and loss statement, and previous years’ tax returns. This can help prove you are a sound credit risk even without a long credit history.

Step 3: Register the car. Once you have signed all of the appropriate paperwork, make sure to register the vehicle to your business and that all paperwork includes the business name. Making sure you do this can help when it comes time to do your business' taxes.

Qualifying for a business car loan is cut and dry if your credit is good and you present a strong reason to the lender as to why you need to purchase a vehicle for your business. Before purchasing a vehicle for your business, have one of our expert mechanics perform a pre-purchase car inspection to make sure it has no hidden problems.